A challenging environment

A backdrop of geopolitical tensions is creating a more challenging environment for equity investors. Conflict and shifting trade policies have disrupted supply chains, while higher funding costs continue to test companies that had previously relied on cheap capital and aggressive buybacks.

Markets have also become increasingly narrative-driven. In recent years, sentiment has rotated rapidly through themes such as US exceptionalism, AI supremacy, AI losers and now energy price exposure. These shifting narratives have amplified volatility and made markets more sensitive to short-term sentiment.

Despite some broadening out in 2025 and prior to the outbreak of the Iran conflict in 2026, concentration also remains a risk. US equities now account for around two-thirds of global indices, and within the US, technology and the so-called ‘Magnificent Seven’ together make up roughly half of the domestic market – up from around 20% a decade ago. This level of concentration has not been seen since the height of the technology bubble in the early 2000s and leaves passive investors heavily exposed to a small group of companies.

In this environment, staying anchored to fundamentals – earnings, balance sheet strength and valuation – is critical and, for investors seeking balanced sources of return, a global, defensive dividend-based approach offers an attractive solution. This can provide access to diverse growth drivers and avoid expensive market segments by focusing on companies that generate consistent cash flows and dividends through market cycles.

Protection in falling markets

Our strategy is designed to perform through cycles by delivering a mix of income and capital appreciation. In normal markets, we aim to outperform through disciplined stock selection and steady income growth. We may lag somewhat during highly speculative rallies, but our focus remains on compounding value over time, rather than chasing short-term momentum. In weaker markets we tend to outperform more strongly, reflecting the resilience of our holdings.

For example, during the market correction in April 2025, the Fidelity Responsible Global Equity Income strategy fell around 9% compared with a 16% decline for the MSCI ACWI, and recovered its losses far more quickly (9 days for the fund versus 59 days for the index). This is very much in keeping with the performance profile we have seen over longer periods, as highlighted in the chart below where we are showing the longer track record of the Fidelity Funds – Global Equity Income Fund which was launched in December 2013.

The strategy also provided some relative protection against a falling market in 2022. The fund fell -3.1% in comparison to a market decline of -8.1%. Market drivers in 2022 included the Ukraine war energy shock, rising inflation, higher rates and recession fears. Some parallels can be drawn with the risks facing investors in 2026, depending on the future path of the Iran conflict.

Defensive characteristics in uncertain markets

Performance is shown for illustrative purposes to demonstrate the fund’s track record. Past performance does not predict future returns. The fund’s returns may increase or decrease as a result of currency fluctuations.

Source: Fidelity International, as at 28 February 2026. Net of fees performance for the Fidelity Funds – Global Equity Income Fund I-ACC-USD share class based on the average of 12 month rolling returns data, calculated on a rolling 12-month period basis since its first full month performance: December 2013. (Fund & share class launch date: 18/11/2013).

A differentiated, diversified approach

In an environment of uncertain growth, we believe sustainable cash generation is becoming a more important differentiator of performance. Dividends provide a tangible and recurring source of return that is typically less volatile than share prices and more closely linked to company fundamentals. Over the past two decades, reinvested dividends have accounted for more than half of the total return from equity markets globally, underscoring their role as a consistent and compounding contributor to long-term wealth creation.

Our all-weather approach targets businesses capable of delivering attractive dividend-based total returns. The portfolio’s focus on resilience rests on three key pillars:

- Business model durability, ensuring companies can generate stable returns through changing market conditions.

- Financial strength, prioritising solid balance sheets and prudent capital allocation.

- Valuation discipline, maintaining a margin of safety by avoiding overvalued or speculative areas of the market.

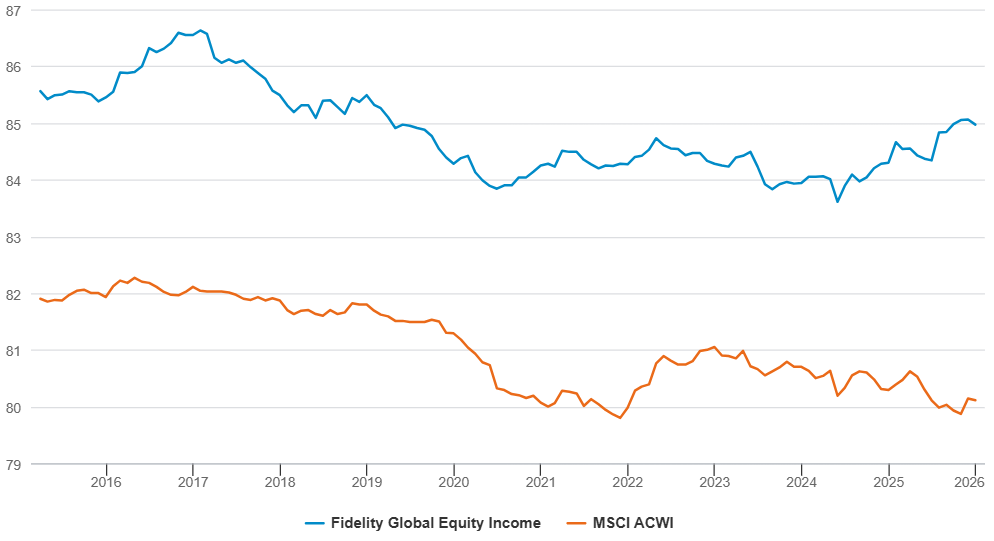

Our focus remains on owning companies with high earnings resilience

Source: Fidelity International, FactSet. Earnings Persistence (5yr) sourced from FactSet, data as at 31 December 2025. In this analysis, the Global Equity Income Strategy uses the Fidelity Funds – Global Equity Income Fund as a representative portfolio due to its longer track. The FactSet Earnings Persistence score is a proprietary measure developed by FactSet that evaluates the consistency and sustainability of a company’s earnings over time. The blue and orange lines in the chart beside show the weighted average of the score for each stock in the FF – Global Equity Income Fund and the MSCI ACWI Index. The portfolio’s higher score indicates higher quality earnings with greater reliability and lower volatility.

Our defensiveness is not built through large allocations to traditional defensive sectors such as staples or utilities, but through genuine diversification. We typically hold between 35 and 45 stocks, with an average holding period of five years that reflects a long-term approach where positioning is driven by stock-specific opportunities rather than top-down themes.

The portfolio’s relatively low exposure to the US (around one-third of holdings), compared with two-thirds of the global index, is not a macro call but the result of careful stock selection. Many of the largest US technology names fall outside of our universe. None of the so-called Magnificent Seven offer dividend yields above 1%. Because the strategy is explicitly designed to deliver income as a meaningful part of total return, every holding must contribute to that objective.

Even if these companies paid higher dividends, most would still not qualify for inclusion because their future cash flows are too uncertain. A large part of the value of some high-profile technology stocks rests on products or services that may take years, or even decades, to develop commercially. The potential outcomes around those assumptions are vast – ranging from significant upside to equally material downside. That degree of uncertainty makes fair value difficult to determine and introduces risks that we seek to mitigate, rather than pursue.

Notably, the portfolio still has meaningful US economic exposure, with around 40% of total sales from portfolio companies generated in the US. This represents a healthy balance: significant participation in the world’s largest economy, without the valuation risk of owning its most expensive companies.

Valuations provide a margin of safety

Another key differentiator is valuation discipline. At an aggregate level, as at end February, the portfolio has a 4.6% Free Cash Flow Yield, compared with 3.5% for the global market, and offers a dividend yield of 2.1% versus 1.6% for the index. This valuation focus provides a margin of safety when sentiment shifts. Expensive segments of the market tend to suffer the sharpest corrections in downturns, while reasonably valued, high-quality businesses can preserve capital and recover more quickly.

Resilient, cash-generative businesses

These principles are reflected in the types of companies we own. Munich Re is a good example of the type of resilient, cash-generative business the portfolio seeks to own. The German reinsurer has raised its dividend every year for more than two decades and outperformed the market by over 100% since the portfolio’s inception. Its steady returns reflect conservative risk management, disciplined capital deployment and a business model that rewards patience and prudence.

The portfolio also includes established UK dividend payers such as Tesco, Unilever and Admiral, each held for its individual merits rather than any top-down view on the domestic economy. Tesco has emerged from a decade of restructuring with a simpler model and renewed competitiveness. Its 3.0% dividend yield, supplemented by share buybacks, positions it well for near double-digit total returns.

This breadth of holdings, spanning financials, industrials, infrastructure and consumer sectors, creates a balanced mix of income and growth drivers that supports performance across different market conditions.

Looking to long-term success

Companies with the financial strength to sustain and grow dividends while continuing to reinvest for future growth are well placed to deliver attractive total returns through different market conditions. Our overarching objective remains unchanged: to deliver strong risk-adjusted returns by investing in resilient companies that combine earnings strength, balance-sheet discipline and valuation support. In an era of geopolitical uncertainty, uneven growth and higher capital costs, those qualities of earnings resilience, financial strength and valuation discipline are likely to define long-term success.

Standard period returns net of fees, GBP (%)

Standard period returns net of fees, GBP (%)

|

1 Month |

3 Months |

Year-To-Date |

1 Year |

3 Years (ann.) |

5 Years (ann.) |

PM tenure (ann.)* |

|

|

FIF IX – Responsible Global Equity Income W-ACC-GBP |

6.5 |

6.0 |

5.8 |

9.2 |

12.7 |

11.8 |

60.0 |

|

MSCI ACWI (N) |

3.4 |

3.9 |

4.3 |

16.3 |

16.6 |

12.6 |

62.2 |

12-month rolling returns, net of fees, in GBP (%)

|

12-month period ending |

Feb-17 |

Feb-18 |

Feb-19 |

Feb-20 |

Feb-21 |

Feb-22 |

Feb-23 |

Feb-24 |

Feb-25 |

Feb-26 |

|

FIF IX – Responsible Global Equity Income W-ACC-GBP |

35.6 |

10.0 |

3.6 |

9.9 |

29.9 |

12.9 |

8.0 |

13.1 |

15.8 |

9.2 |

|

MSCI ACWI (N) |

36.8 |

7.3 |

2.8 |

8.2 |

19.0 |

12.3 |

1.7 |

17.9 |

15.6 |

16.3 |

Past performance does not predict future returns. The fund’s returns may increase or decrease as a result of currency fluctuations.

Source: Fidelity International, 28 February 2026. All returns for FIF IX – Responsible Global Equity Income W-ACC-GBP. Basis: bid-bid, gross income reinvested in GBP terms. Index is MSCI ACWI (net). *Aditya Shivram was appointed portfolio manager on 1 July 2021. Performance is annualised. The performance figures above include performance prior to the repurpose of the fund on 18 March 2022 from the legacy Fidelity Institutional Funds – Global Focus Fund. Before this date the performance was achieved in circumstances that no longer apply.

Learn more about the Fidelity Responsible Global Equity Income Fund

Important information

This is for investment professionals only and should not be relied upon by private investors. Investors should note that the views expressed may no longer be current and may have already been acted upon. Past performance does not predict future returns. Returns may increase or decrease as a result of currency fluctuations. The value of investments and the income from them can go down as well as up so you may get back less than you invest. The value of investments in overseas markets can be affected by changes in currency exchange rates. Investments in emerging markets can be more volatile than other more developed markets. Reference to specific securities should not be construed as a recommendation to buy or sell these securities and is included for the purposes of illustration only. The Key Investor Information Document (KIID) is available in English and can be obtained from our website at www.fidelityinternational.com. The Prospectus may also be obtained from Fidelity. Issued by FIL Pensions Management. Authorised and regulated by the Financial Conduct Authority. GCT260375EUR

![]()

Read the full article here