Updated on June 28th, 2024 by Bob Ciura

Antero Midstream (AM) stock currently has an attractive dividend yield of 6.0%. It is one of the high-yield stocks in our database.

We have created a spreadsheet of stocks (and closely related REITs and MLPs, etc.) with dividend yields of 5% or more.

Antero is part of our ‘High Dividend 50’ series, where we cover the 50 highest yielding stocks in the Sure Analysis Research Database.

You can download your free full list of all high dividend stocks with 5%+ yields (along with important financial metrics such as dividend yield and payout ratio) by clicking on the link below:

In this article, we will analyze the prospects of Antero Midstream.

Business Overview

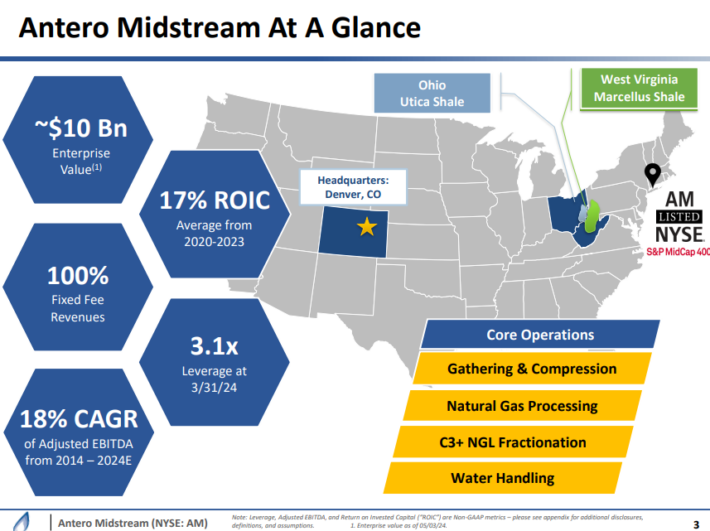

Antero Midstream Corporation is a midstream company providing gathering and compression, processing and fractionation, and pipeline services on a captive basis to Antero Resources (AR).

AR is the 5th largest natural gas producer and 2nd largest NGL producer in the country, operating fields primarily in West Virginia.

As seems typical for these midstream businesses, the publicly traded entity is a pass-through for the profits from the underlying operating entity.

Source: Investor Presentation

In the 2024 first quarter, Antero Midstream’s gathering and processing volumes increased 4% and 6% respectively compared to the prior year quarter.

Net income reached a company record of $104 million, or $0.21 per diluted share, marking a 17% per share increase from the previous year quarter.

Adjusted EBITDA also increased by 10% compared to the prior year quarter. Capital expenditures decreased by 11% from the prior year quarter.

Revenue for the first quarter was $279 million, with significant contributions from the Gathering and Processing segment and the Water Handling segment.

Growth Prospects

Antero Midstream’s primary growth catalyst moving forward is paying down its debt, which it plans to do aggressively in the coming years. In the 2024 first quarter AM’s leverage declined to 3.1x, down from 3.3x at the end of 2023.

It has also completed a fairly aggressive capital spending program and these projects are now coming online, generating increased EBITDA.

It also may continue to opportunistically pursue small growth projects as they become available to it through its close partnership with Antero Resources.

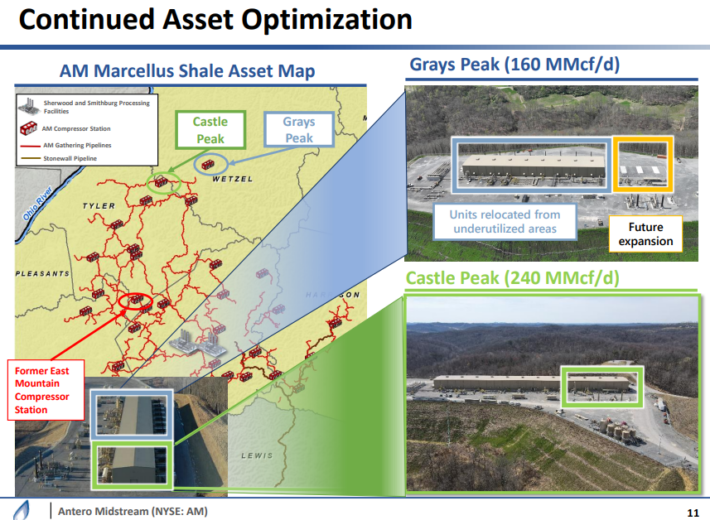

Antero Midstream is also investing in growth through optimizing its asset footprint.

Source: Investor Presentation

For example, in the first quarter the company placed the Grays Peak compressor station into service with an initial capacity of 160 million cubic feet per day.

Otherwise, it will look to increase dividend per share payouts and/or buy back shares if they remain attractively priced. Antero currently has a $500 million share repurchase authorization in place.

Buying back shares will serve as a growth catalyst by reducing the total share count, thereby increasing distributable cash flow per share over time.

Competitive Advantages

Antero Midstream’s primary competitive advantages are found in its multi-decade underlying inventory via its partnership with Antero Resources, its just-in-time approach to capital investments, and its peer leading returns on invested capital.

It is the primary midstream service provider to Antero Resources, a company with a premium core drilling inventory that exceeds 20 years.

Its just-in-time and flexible capital investment philosophy helps it to minimize risks on its capital expenditures while also minimizing the time from spend to cash flow on its growth projects.

As a result, it is able to generate consistent and repeatable organic growth along with peer-leading returns on invested capital.

Dividend Analysis

Antero Midstream is unlikely to grow its dividend in 2024, as management is laser focused on deleveraging the balance sheet right now. Fortunately, the company has no near-term maturities in 2024 or 2025.

Once it achieves its leverage target of at or below 3.0x (expected by the end of 2024), it could increase the dividend, or continue to further pay down debt, depending on market and industry conditions at the time.

However, given the 6% current dividend yield, there is no need for dividend growth to generate an attractive yield, and the dividend appears to be quite safe as well.

AM has a projected dividend payout ratio of 53% for 2024, which indicates a secure dividend.

Final Thoughts

Antero Midstream is one of the cheapest C-Corp midstream companies in the market today, and also offers a very attractive dividend yield that appears safe for many years to come.

It has a stable, commodity price resistant cash flow profile with a long demand timeline ahead of it. Furthermore, its main counter-party is rapidly deleveraging its balance sheet, further strengthening Antero Midstream’s safety profile.

While Antero Midstream is unlikely to be a rapid grower of its cash flow or its dividend in the coming few years, we view AM stock as attractive for income investors.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

Other Sure Dividend Resources

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].