“Those who stand for nothing fall for anything.”

Alexander Hamilton, first US Secretary of the Treasury

In Act 1, Scene 2 of William Shakespeare’s play, Julius Caesar, a soothsayer warned Caesar to, “Beware the Ides of March.” But Caesar failed to heed this advice, and he was assassinated on March 15th in the year BCE 44. More than 400 years after Shakespeare penned this phrase, people still associate the Ides of March with impending doom. Vanguard’s former OCIO clients would be wise to follow this tradition.

Trustees Are no Longer Protected by the Spirit of Jack Bogle

On March 15, Mercer, a division of Marsh McLennan, completed its acquisition of Vanguard’s outsourced chief investment officer (OCIO) business. Most of the Vanguard clients who are moving over to Mercer are large institutions including endowments, foundations, and nonprofits. The transaction seemed odd to me, given that Mercer’s traditional investment consulting and OCIO services have a penchant for active managers and alternative investments.

My fear is that Vanguard’s propensity for low-cost index funds over higher-fee active funds and expensive alternative investments will not survive in its OCIO practice under Mercer.

In a June 4 interview with Pensions & Investments (P&I), Mercer’s US CIO Olaolu Aganga noted that Vanguard’s OCIO clients will have access to the full spectrum of passive and active strategies on Mercer’s platform, including alternative investments. In her interview with P&I, she stressed Mercer’s breadth and depth of offerings in the form of fund of funds including real estate, private credit, infrastructure, private equity and secondaries, as well as co-investments and venture capital.

The problem I have with this is that there is a preponderance of evidence – which many investors continue to reject – that very few active managers are capable of consistently outperforming inexpensive index funds. There is similar evidence that alternative investments do not add value to institutional portfolios. It especially concerned me when Aganga called out hedge funds specifically as another opportunity now opened to Vanguard OCIO clients, despite the overwhelming evidence that hedge funds are not beneficial for most institutional investors.

Adding to my concern is the fact that, in my experience, when OCIOs and investment consultants present trustees with “new opportunities,” they routinely frame them in a way that overstates the benefits, understates the risks, discounts the skills required to succeed, and all but ignore incrementally higher costs.

A Brief History of Vanguard Index Funds

In 1976, Jack Bogle, founder of the Vanguard Group, launched the Vanguard 500 Index Fund. Unlike every other mutual fund at the time, the fund’s objective was to simply replicate the performance of the S&P 500 index. This was a highly unconventional approach, even though it conformed with well-established mathematical principles and supporting evidence that most active managers are unlikely to outperform a comparable index.

In fact, only a few years earlier, Eugene Fama published a groundbreaking paper on the efficient market hypothesis (EMH). Fama presented a compelling case that securities prices incorporate all publicly available information, thus preventing investors from identifying and profiting from mispriced securities. This implied that investing in low-cost funds was the most sensible approach for nearly all investors.

The Vanguard Group was the first to commercialize the index fund on a large scale. Starting with only $11 million in 1976, the fund grew rapidly. Over time, its performance validated the EMH: most actively managed funds failed to keep pace with the Vanguard 500 Index Fund. Building on its success, Vanguard soon applied the indexing philosophy in other securities markets including fixed income, international equity, and real estate investment trusts (REITs). Results were predictably similar.

Something Old and Something New: The Outsourced Chief Investment Officer

“Financial operations do not lend themselves to innovation. What is recurrently so described is, without exception, a small variation on an established design, one that owes its distinctive character to the aforementioned brevity of financial memory. The world of finance hails the invention of the wheel over and over again, often in a slightly more unstable version.”

John Kenneth Galbraith, financial historian

In the early 2000s, a new investment advisory model took the institutional investment plan market by storm. The model, referred to as an OCIO, was, in the words of John Kenneth Galbraith, “a small variation on an established design.” The variation was the creation of complex portfolios that relied heavily on active managers and allocations to alternative investments, such as private equity, hedge funds, and venture capital. The rationale for this approach was based largely on the exceptional performance of the Yale University Endowment. OCIOs argued that replicating Yale’s allocation would likely produce similar results.

The “established design” was simply the concept of discretionary management. Prior to the emergence of OCIOs, institutional investment plan trustees relied primarily on non-discretionary advice offered by investment consulting firms.

The reintroduction of discretionary management seemed like a novelty only because few trustees recalled that consulting firms persuaded them to abandon it in the 1970s and 1980s. At the time, consulting firms were hired to provide independent performance reporting, and their reports revealed that discretionary advisory services offered by bank asset management departments failed to provide sufficient value to justify the higher fees.

Despite the history, many trustees bought into the OCIO concept because they believed that the higher fees were justified by the superior, Yale-like strategies that OCIOs offered. Few trustees understood that the real secret of Yale’s success was not simply a function of a blunt asset allocation strategy. Instead, it was the presence of a unique investment ecosystem that combined excellence in governance, people management, mentorship, and access. The essential replication of this ecosystem was conveniently absent from OCIO sales pitches.

Over the last 24 years, assets under management (AUM) of OCIOs increased from almost nothing to nearly $2 trillion at the end of 2023. As is always the case, rapid growth attracted many new market entrants. Investment teams at large endowments left to launch new firms such as Investure, Global Endowment Management, Morgan Creek, and others. Investment consulting firms such as Verus, Callan, and NEPC launched OCIO services of their own. This was especially ironic because investment consulting firms had advised trustees to abandon discretionary, bank asset management departments several decades earlier.

The Vanguard Group also began offering discretionary asset management services to institutional plans in the early 2000s, although it was not officially referred to as an OCIO service until the late 2010s. Like traditional OCIOs, Vanguard’s AUM grew rapidly to $54.7 billion by the beginning of this year.

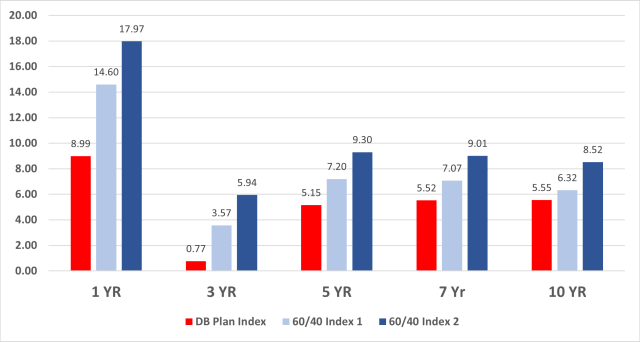

Unfortunately, the extraordinary growth of OCIO assets was not accompanied by impressive performance. Figure 1 shows multiple trailing periods of OCIO-managed defined benefit plans versus two indices comprising 60% equities and 40% bonds. The OCIO Index underperformed both 60/40 indexes by substantial amounts in all trailing periods.

Exhibit 1. OCIO Defined Benefit Pensions Plans Index Annualized Returns (%) through March 31, 2024.

Source: March 31, 2024, Alpha Capital Management & NASDAQ OCIO Indices. https://www.alphacapitalmgmt.com/ocioindex.html.

The failure of OCIOs to keep pace with a simple, low-cost strategy is tragic but unsurprising. All OCIO investment strategies are grounded on two fundamentally flawed assumptions. The first is that efficient markets can be easily outmaneuvered in traditional asset classes. The second is that Yale’s performance in alternative asset classes can be easily replicated. Neither is true.

The poor performance of most OCIOs is what made Vanguard’s OCIO practice so special. It offered a rare haven for trustees who sought refuge from the folly of active management and alternative investments. Now, this haven may disappear.

Mercer Hoists a Red Flag on the HMS Vanguard

“You either have the passive strategy that wins the majority of the time, or you have this very active strategy that beats the market…For almost all institutions and individuals, the simple approach is best.”

David Swensen, former CIO of the Yale Investments Office (2012)

Bogle named the Vanguard Group after the famous British ship, the HMS Vanguard. In 1798, the ship played a key role in the British navy’s victory over the French fleet in the historic Battle of the Nile. The HMS Vanguard also served in the Napoleonic wars, but it was eventually repurposed into a prison ship in 1812. By 1821, the HMS Vanguard reached the end of its useful life, and it was dismantled for scrap.

Despite initial concerns regarding Mercer’s acquisition of Vanguard’s OCIO practice, the transaction is not necessarily problematic. If Mercer signals a clear and enduring commitment to honor trustees’ past decisions and refrains from pushing active managers and alternative investments, it is conceivable that Mercer’s scale will enable clients to benefit from lower costs. But the P&I interview with Mercer’s Aganga seems to signal otherwise.

To understand my concern, it is important to recognize that not only does Mercer encourage clients to employ investment strategies that evidence shows are unlikely to add value — just as many other OCIOs do — but the firm also suffers from a tremendous burden of size.

In 1963, the founder of the value investing philosophy, Ben Graham, warned financial analysts that it is nearly impossible to beat the market when you effectively are the market. As of June 2023, Mercer had $16.2 trillion of assets under advisement or under management in its combined investment consulting and OCIO practices.

Whatever inefficiency exists in securities markets, it is nowhere near $16.2 trillion. Mercer may not be the entire market, but the firm has a large enough chunk to impair any chance of exploiting these inefficiencies to benefit their entire client base. Sure, some clients will get lucky at least in the short term, but the unforgiving math of market efficiency will catch up to most of them eventually.

Vanguard’s former OCIO clients already decided that heavy reliance on index funds would maximize their chances of achieving their long-term objectives. This decision is supported by compelling evidence that using active managers and alternative investments is highly unlikely to provide sufficient rewards. If Mercer reintroduces these new opportunities, they are dismissing trustees’ decisions and abandoning Bogle’s philosophy.

In fairness to Mercer, it is hardly alone in encouraging trustees to embrace investment strategies that are unlikely to reward them for incrementally higher fees. But I believe that this case is considerably more tragic because of the prudence of the strategies that Vanguard’s former OCIO clients currently have in place.

Wisdom from Swensen and Buffet

On May 5, 2021, David Swensen, the famed CIO of the Yale Investments Office, passed away. During his 36 years at the helm of the Yale University Endowment, he outperformed his peers. This feat required him to traverse a dense minefield of investment, governance, and management challenges. In a January 2012 speech — which ironically took place at the John C. Bogle Legacy Forum honoring Vanguard’s founder — Swensen reflected on the rarity of Yale’s accomplishment and concluded that it was impossible to replicate.

Rather than advising his peers to embark on similarly unlikely quests, he advised them to circumvent the minefield entirely by following a simpler, less expensive, and refreshingly unconventional path that would likely bring them to a similar destination. He concluded that nearly all institutional and individual investors would be better off investing exclusively in low-cost index funds. Warren Buffett reached a similar conclusion and stated as much in his 1996 annual letter to shareholders.

Vanguard’s former OCIO clients wisely adhered to Swensen’s and Buffett’s advice. They concluded, based on a preponderance of evidence, that their approach was in the best interest of their beneficiaries. Their courage is commendable because, despite the undeniable merits, an all-indexed strategy remains highly unconventional. Mercer should respect the logic, prudence, and courage of their newly acquired clients. If they don’t, trustees should replace them with somebody who will.