In the aftermath of the latest May series of marquee art auctions in New York and Sotheby’s record-breaking £296.3m sale of 20th century masterworks from the collection of the Bahamas-based billionaire Joe Lewis in London in June, market insiders and commentators were understandably keen to draw upbeat general conclusions from what appeared to be encouragingly positive results.

“It’s good for everyone,” said Alex Lachmann, a Russian collector based in London, after Sotheby’s racked up £393.4m (with fees) from its two-part June modern and contemporary sale, the highest total ever achieved in a single night of auctions in Europe. “The spirit is different from before. People are spending money to put together good collections,” Lachmann added.

Back in May, Sotheby’s, Christie’s and Phillips raised an aggregate $2.5bn (with fees) from their New York sales from their various evening and day sales, almost double the $1.3bn that the auction houses had achieved the previous May. It was the companies’ best collective performance in New York since November 2022, when Christie’s $1.5bn Paul Allen sale helped push the takings up to $3.2bn.

“We’re really in a trend reversal,” says Thierry Ehrmann, the head of the French auction result database Artprice. “The art market has returned to a level of solid health without runaway enthusiasm, which makes sense in this turbulent economic and geopolitical environment.”

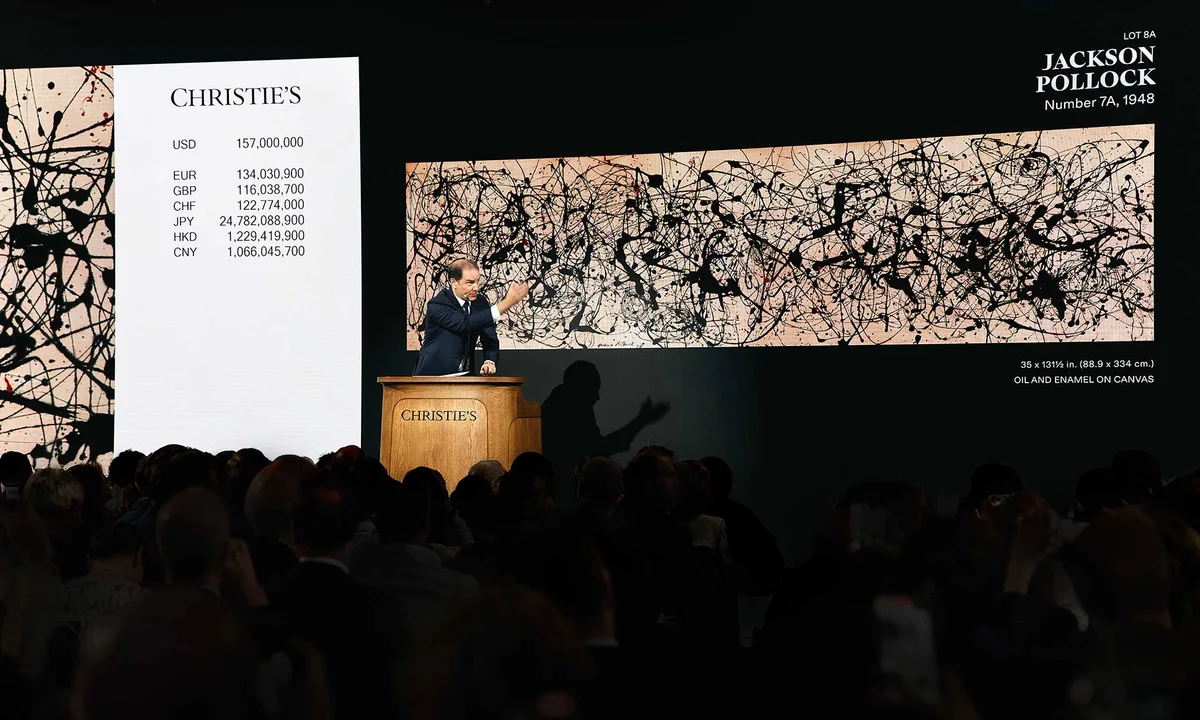

This time round, most of the truly spectacular prices were achieved at Christie’s evening sale of 20th-century art, where 16 masterworks from the collection of S.I. Newhouse racked up $630.8m, led by the $181.2m given for Jackson Pollock’s 1948 drip painting Number 7A and the $107.6m for Constantin Brâncuși’s 1913 sculpture, Danae. There was a further $98.4m for the 1964 Mark Rothko abstract No. 15 (Two Greens and Red Stripe) from the estate of the admired New York collector Agnes Gund. All three results were auction records for the artists.

“Despite two international wars—at least—still unresolved, the K-shaped economy seems to have virtually no top-side limit,” enthused the influential New York art adviser and market commentator Josh Baer. “Tonight’s result will stimulate all levels of the art market.”

This is a familiar narrative. The art market is cyclical. It goes through dips after economic or geopolitical crises. Demand and supply temporarily dry up, then flow again. Renewed confidence at the top trickles down through every level. After all, people with spare money will always buy art—so the story goes.

But then, in early June, we read in The New York Times that Pace, one of the quartet of international mega-dealerships, is laying off 50 of its staff and 50 of its artists. “The whole art gallery art system became too big, too commercial, too impersonal and too corporate,” Marc Glimcher, Pace’s chief executive, told the Times. “We all know it’s true.”

As has been widely reported, the soaring costs of running bricks-and-mortar galleries and participating in art fairs have put pressure on dealerships at every level of the trade since Covid-19, resulting in a spate of closures. In June, Dépendance in Brussels and Tiwani Contemporary in London were added to the ever-lengthening list of casualties.

“It’s the worst business model on the planet,” says Marc Straus, a New York contemporary gallerist who operates two spaces in Manhattan. “Rents are way up and the cost of shipping has tripled,” according to Straus, a former oncologist who founded his dealership in 2011 and who was the first gallerist to show Jeffrey Gibson, who represented the US at the 2024 Venice Biennale. “There’s huge hesitation right now. Older collectors are on pause,” Straus adds, after what he describes as the “crazy speculation” in ultra-contemporary artists in the early 2020s. “The prices went up absurdly. Pretty much all of that has collapsed. I think much of the population is focused elsewhere at the moment.”

So, what is going on? Clearly, a major bifurcation seems to be developing between sales at the gleaming top end of the auction market and those achieved by dealers in bricks-and-mortar galleries.

Steady flow to auction

Boomer-generation collectors are dying or downsizing, providing a steady flow of big-ticket works to auction, and the houses still have enough wealthy clients on their books to ensure that they sell. Backstage dealmaking and judicious withdrawals ensure that 100% successful “white-glove” sales have become routine at the top level of the auction market. Thanks to guarantees, sales are predictable, but few lots sell over estimate. This May in New York, a record 79% of the turnover at Christie’s, Sotheby’s and Phillips’s evening auctions was generated by lots covered by guarantees from third parties, according to data supplied by the London-based auction analysts Pi-eX.

“The art market is increasingly behaving like the stock market, with performance at the top end appearing disconnected from wider economic indicators, particularly weak consumer confidence in the US,” says Christine Bourron, the founder of Pi-eX. Yet Bourron also points out that though the results for these May sales were the highest for three years, the totals were still well below the levels the houses achieved in this series in 2014, 2015 and 2019. Between May 2014 and May 2026, the value of the S&P 500 share index increased by over 280%.

Patrick Heron’s Christmas Eve: 1951 was shown at Hazlitt Holland-Hibbert during LGW © Estate of Patrick Heron © DALiM

It would seem that hoarding, rather than spending, has become a defining characteristic of the tax-averse ultra-rich in recent years. The Financial Times recently reported that the “global flight of the wealthy” had slowed sharply as political and tax concerns had eased. Only a quarter of the rich people surveyed by Capgemini said they had changed or intended to change their main tax residence in 2025, down from 56% in 2024. If the ultra-rich sit on their wealth like dragons on piles of gold, rather than let it trickle down into the wider economy by splashing out on luxury items like art, this isn’t great news for either auction houses or dealers.

Blue-chip 20th century art might have sold for plenty of money at the £393.3m Lewis sale, but it took noticeably longer for Sotheby’s ultra-wealthy clients to spend it. Time and again billionaires on telephones were taking a minute or two to decide to bid £50,000 or £100,000 on multimillion pound lots. Auctioneer Oliver Barker spent 15 minutes taking split bid after split bid on an Egon Schiele painting that eventually sold for a within-estimate £17.9m. The dragons are minding their gold.

There is plenty of publicly available data that confirms the performance of the auction market. Dealer sales, on the other hand, are confidential and those trying to make sense of what is going on in that sector of the art world have to rely on anecdotal evidence.

At this year’s June edition of the Art Basel fair in Switzerland—the traditional global centerpiece of the gallery trade in modern and contemporary art—much was made of the international mega-dealership Hauser & Wirth selling the 1963 Picasso canvas, The Painter and His Model in a Landscape, for $35m, among more than 30 works on the first VIP preview day.

But hadn’t the market changed? “The market is always changing,” countered Iwan Wirth, co-founder of the gallery, keen to create a sense of the art market going through its usual business cycles.

But on the second day of the VIP preview, the attendance was noticeably thin. Shockingly, there were hardly any queues at Art Basel’s famously popular wurst stalls. It has become common anecdotal knowledge that many American collectors now prefer to visit Art Basel Paris in October, rather than the fair group’s home fixture in Switzerland in June.

“I can’t remember a greater moment of uncertainty, what with wars, the state of the economy and generational shifts. We’re experiencing a sea change. We’ve had a good run, but things aren’t easy,” says James Holland-Hibbert, the director of the London-based gallery Hazlitt Holland-Hibbert. Founded in 2002 in St James’s, the dealership put together a stand-out exhibition (until 10 July) of 23 paintings by Patrick Heron from the early 1950s for London Gallery Weekend (LGW) in early June. These include Heron’s early, pre-abstract masterwork, Christmas Eve: 1951 (1951), made for the Festival of Britain, priced at £1.2m. “I sometimes think running a retail premises is hard to justify,” says Holland-Hibbert, who cites the combination fairs, advisers and Artnet as reducing the footfall of collectors into his gallery in recent years.

Gallery focus

The sixth edition of LGW, featuring more than 120 participants, put a welcome focus back on bricks-and-mortar dealerships at a time when so much media attention is devoted to auctions and fairs.

New York-based Lehmann Maupin, which has a permanent spot in Frieze’s gallery hub at No. 9 Cork Street, rather than taking on the expense of a standalone space, showed how dealers can adapt to today’s tough trading conditions. The gallery is showing recent paintings by the London-based artist Anna Freeman Bentley (until 14 August), who studied at the Royal College of Art with Caroline Walker. The two painters share a similar visual language but, unlike Walker, whose works have sold for more than £900,000 at auction, Bentley has had little secondary-market exposure. By the Friday morning of LGW, at least half the works had found buyers or reserves for prices from £10,000 to £70,000, a price point that has become a sweet spot for emerging artists.

During a panel discussion at No. 9 Cork Street on the Friday of LGW, the east London contemporary dealer Kate MacGarry talked of how “so many challenges continue to bash small businesses like galleries”. On the other side of the road, Tiwani Contemporary, a gallery dedicated to African art, had just shuttered, following the closure of Cork Street’s Stephen Friedman Gallery in February. “We have to find another story,” said MacGarry.

Knowledgeable insiders often say that the art trade is not just one market, but several. A single season of better auction results in London and New York isn’t going to transform the fortunes of the entire business. Fewer and fewer people believe any more in the neoliberal story of trickle-down economics. But as we enter a new era of forever wars and continuous, social media-fuelled anxiety, is the virtuously cyclical nature of the art trade turning out to be just another story, too?